Public equity markets are undergoing significant structural changes driven by technological advancements, regulatory developments, and shifts in market participant behavior. Furthermore, markets are evolving at an accelerated pace given the dramatic growth in passive instruments, increased algorithmic trading and the use of trading bots, among other developments. As markets continue to transform, investors find themselves navigating an increasingly complex and interconnected landscape that produces price discrepancies that are evolving and dynamic.

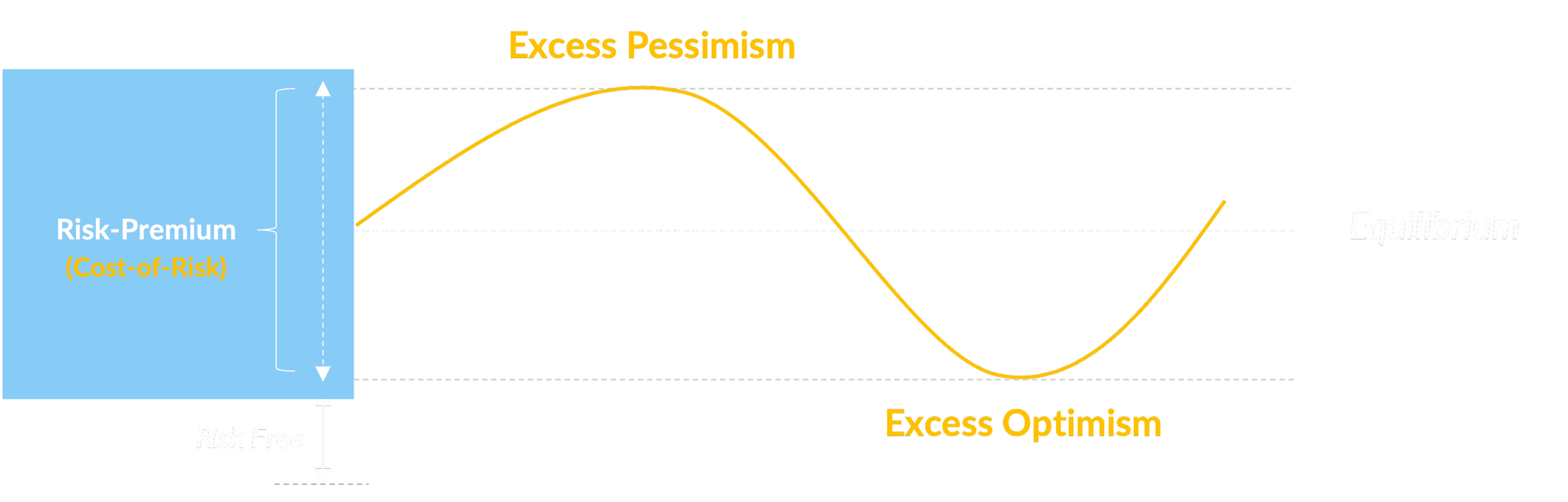

Similarly, we observe that the market doesn’t serve every investor equally, occasionally accruing value and wealth for some while passing the bill along to others. In buoyant markets, investors tend to chase performance, ultimately acquiring securities that reflect excess optimism. During market downturns, they gravitate to options they perceive as lower-risk, thus contributing to an excess of pessimism in segments of the market. These behaviors amount to buying and selling risk premiums at inopportune moments, diminishing returns and hindering investors from seizing attractive opportunities.

We exploit modern drivers of pricing inefficiency by measuring and contextualizing the Cost-of-Risk - the premium investors require to embrace uncertainty.

Frustrating as these trends are for many active managers, particularly for those entrenched in processes that were designed for markets past, we believe these new market dynamics actually present significant opportunity for those capable of identifying and leveraging the resulting inefficiencies in asset pricing.

As long-time fundamental investors, we have developed an investment process that enhances our research with internally developed tools that we believe are innovative and efficient at exploiting pricing inefficiencies driven by evolutions in the market.

Please click here to learn more about our Methodology.